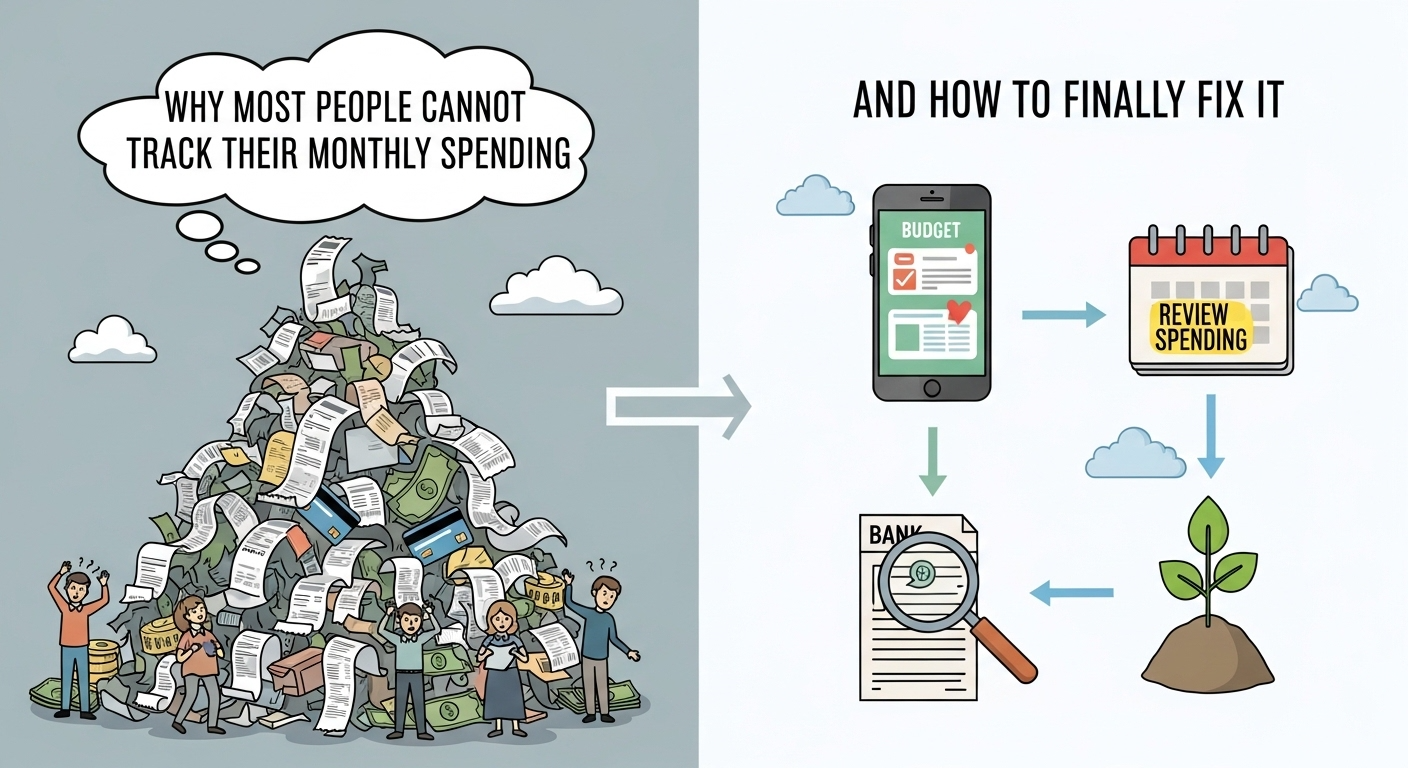

Why Most People Cannot Track Their Monthly Spending — And How to Finally Fix It

You sit down at the end of the month, open your bank app, and feel a familiar sinking feeling. The number staring back at you is lower than it should be. You spent more than you planned — again — and you cannot quite explain where it all went. If this sounds familiar, you are in very good company. Most people struggle to accurately track their monthly spending, and the reasons go deeper than simple carelessness.

The Real Reason Money Disappears Without a Trace

The most significant shift in how people spend money over the past decade is also the most overlooked cause of poor spending awareness: cash has almost disappeared from daily life.

When you hand over physical notes and coins, your brain registers a genuine loss. The transaction feels real because something tangible leaves your hand. Tapping a card or clicking a button produces no such sensation. The money moves, but your brain barely notices.

Financial analyst Sarah Johnson puts it plainly — when paying by card, it simply does not feel like spending real money. That psychological disconnect is not a personal failing. It is how human brains respond to abstract versus concrete experiences. Digital payments are designed for frictionless convenience, and that convenience comes at the cost of financial awareness.

Layered on top of that is the explosion of subscription services, automatic renewals, and one-click purchases. A significant portion of most people’s monthly spending now happens on autopilot — charged quietly in the background without any active decision being made at the moment of payment. Those $12, $15, and $20 monthly charges accumulate into hundreds of dollars before most people even think to check.

The Instant Gratification Trap

Beyond the mechanics of digital payment, there is a deeper behavioural force at work. Modern life is structured around immediate reward. Same-day delivery, instant streaming, one-tap food ordering — every system around us is optimised to reduce the gap between wanting something and having it.

Behavioural economist Dr. Emily Schultz notes that this cultural emphasis on instant satisfaction pulls decision-making away from long-term thinking. When the pleasure of a purchase is immediate and the financial consequence feels distant and abstract, the brain consistently underweights the financial side of the equation.

The result is a pattern most people recognise in themselves: spending decisions made in the moment based on how something feels, rather than whether it fits a broader plan. Each individual decision seems reasonable. The cumulative effect is a monthly total that feels inexplicable.

Why Emotions Make It Worse

Money is not a neutral topic for most people. It carries weight — anxiety, guilt, shame, aspiration, status. Clinical psychologist Dr. Sophia Hernandez points out that many people avoid examining their finances closely precisely because they do not want to confront what they will find.

This emotional avoidance creates a self-reinforcing cycle. Avoiding the numbers means not knowing the reality. Not knowing the reality makes it easier to keep spending without confronting the consequences. When the monthly total eventually becomes impossible to ignore, the emotional discomfort is greater — which makes avoidance feel even more appealing next time.

Understanding that this is a psychological pattern rather than a personal character flaw is genuinely useful. It means the solution is not simply trying harder — it is changing the system so that emotional avoidance has less opportunity to take hold.

Practical Ways to Actually Fix This

The good news is that none of this requires willpower or dramatic lifestyle changes. Small structural adjustments consistently outperform motivation-based approaches to financial tracking.

Use a budgeting app that connects to your accounts. Tools like YNAB, Mint, or your bank’s own categorisation features do the work of recording transactions automatically. The key is reviewing what they capture regularly — even ten minutes once a week is enough to stay aware of patterns before they become problems.

Set a weekly review appointment with yourself. Irregular reviews mean problems compound unnoticed. A fixed ten-minute slot each week — Sunday evening, Monday morning, whatever works — creates a rhythm that prevents month-end surprises.

Audit your subscriptions every three months. Write down every recurring charge on your accounts. Most people find at least two or three services they had forgotten about or stopped using. Cancelling unused subscriptions is the easiest money most people will ever save.

Introduce a waiting period for non-essential purchases. A 24 to 48-hour pause before buying anything above a set threshold — $30, $50, whatever feels right — dramatically reduces impulse spending without requiring ongoing willpower. Many purchases simply stop feeling necessary after a night’s sleep.

Automate savings before you can spend. Setting up an automatic transfer to a savings account on payday removes the money before spending decisions are made. You adapt your spending to what remains rather than trying to save whatever is left over — which, for most people, is nothing.

The Mental Barriers Worth Knowing About

| Barrier | What It Looks Like | How to Address It |

|---|---|---|

| Emotional avoidance | Avoiding checking accounts or statements | Start with just one account, once a week |

| Impulse control | Buying before thinking | Implement a 24-hour rule for non-essentials |

| Feeling overwhelmed | Thinking tracking is too complicated | Start with one simple category only |

| Lack of motivation | Not seeing the point | Connect tracking to a specific goal |

What Financial Awareness Actually Gives You

The point of tracking spending is not restriction or deprivation. It is clarity — and clarity produces options that ignorance does not.

When you know where your money goes, you can make deliberate choices about whether that is where you want it to go. You can identify spending that genuinely adds to your life and cut spending that happens out of habit or inertia. You can direct money toward goals that matter to you rather than watching it disappear into subscriptions and impulse purchases.

Financial coach Olivia Sanchez frames it well: tracking expenses is about empowerment and freedom, not deprivation. Knowing where your money goes lets you align spending with your actual values — and that alignment is what financial peace of mind actually feels like.

FAQs

Q: How long does it take to set up a basic expense tracking system? A: An initial setup of 30 to 60 minutes — connecting accounts to an app or setting up a simple spreadsheet — is enough to get started. Ongoing maintenance is typically ten minutes per week.

Q: What is the best app for tracking spending? A: YNAB, Mint, and Personal Capital are widely used options. Many banks now offer built-in categorisation tools that are sufficient for most people without needing a separate app.

Q: Is it better to track manually or use an app? A: Apps reduce friction and are more likely to be maintained consistently. Manual tracking works well for people who find the act of writing things down creates better awareness — the best method is whichever one you will actually use.

Q: How do I deal with the emotional side of reviewing my spending? A: Start without judgement — treat the first few reviews as data collection rather than self-assessment. The goal is awareness, not punishment. Patterns become easier to address once they are visible and normalised rather than shameful.

Q: How often should I review my spending? A: Weekly reviews prevent surprises and take far less time than monthly catch-ups. A ten-minute weekly check is more effective than an hour-long monthly review.

Q: What is the single most impactful first step? A: Auditing your subscriptions. It takes fifteen minutes, costs nothing, and almost always reveals money being spent on things you no longer use or need.

This article is for general informational purposes only and does not constitute financial advice. For guidance specific to your financial situation, consult a registered financial adviser.