Australia Retirement Policy Shift 2026 — Future of Pension Age Under Government Review

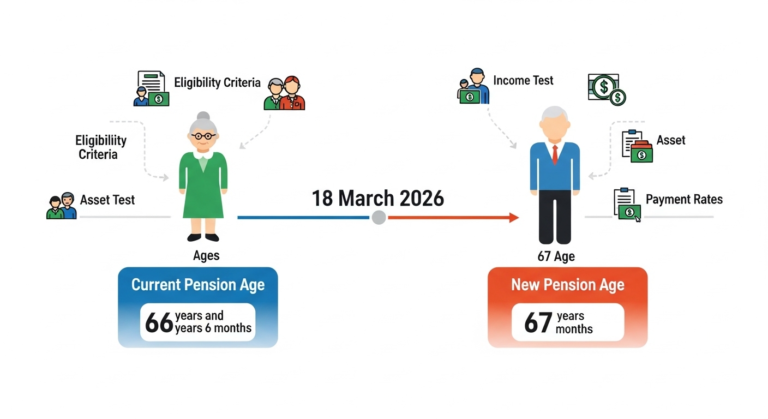

For decades, 65 was the number Australians carried in their minds as the retirement milestone. The point at which work wound down, the Age Pension became accessible, and a different chapter of life began. That assumption no longer holds. By 2026, the Age Pension eligibility age has been raised to 67 for both men and women, and Australians who had built their retirement planning around the old benchmark are navigating a landscape that requires considerably more flexibility than previous generations needed.

The shift is not sudden in 2026. It has been arriving incrementally since 2017, moving through a series of staged increases that have brought the qualifying age from 65 to its current level. But for the Australians caught in the transition, particularly those now approaching their mid-sixties with plans built around earlier assumptions, the practical consequences are immediate and personal.

How the Pension Age Arrived at 67

The movement from 65 to 67 has been a staged process spanning nearly a decade, with each step representing a six-month increment applied to progressively younger birth cohorts.

| Period | Age Pension Eligibility Age |

|---|---|

| Before 2017 | 65 |

| 2017 to 2019 | 65.5 to 66 |

| 2019 to 2021 | 66 |

| 2021 to 2023 | 66.5 |

| 2023 onward including 2026 | 67 |

Australians born on or after 1 January 1957 must wait until 67 to claim the Age Pension. As of 2026, no further increase beyond 67 has been legislated, meaning the current threshold is confirmed for the foreseeable planning horizon. But the review being conducted of broader retirement policy settings means that the longer-term picture remains a subject of active policy discussion.

Why the Change Was Made

The increase to 67 responds to pressures that are demographic and fiscal simultaneously, and both dimensions reinforce each other in ways that make the policy logic difficult to dispute even for those who find the personal consequences difficult to manage.

Australia’s population is ageing at a pace that is measurable in projections with significant consequences for public finances. Around 22 percent of Australians are projected to be aged 65 or over by 2066, up from a considerably smaller proportion when the original pension age was established. Average life expectancy now exceeds 83 years, meaning the typical Age Pension recipient collects payments across a considerably longer period than the system was originally designed to support.

The Department of Social Services has framed the reform explicitly around sustainability and workforce participation. A pension age that reflects modern life expectancy and improved health outcomes in later life is more fiscally sustainable than one calibrated to the demographic realities of a previous century. The goal is to reduce long-term fiscal strain while acknowledging that many Australians are capable of workforce participation well into their late sixties.

The secondary effect, increased workforce participation among older Australians, is visible in the data. Australian Bureau of Statistics figures show that participation rates for those aged 65 to 69 have more than doubled in the past two decades. Employers have responded with more flexible arrangements, phased retirement options, part-time roles, and retraining programs that did not exist at scale when the workforce expectation was complete cessation of work at 65.

The Real Experience of People in Transition

The policy rationale is coherent in the aggregate. But it lands differently on individuals navigating the gap between when they expected to retire and when the pension becomes available.

Margaret Lawson, 64, from Brisbane, built her retirement expectations around a timeline that the policy shift has moved. She now faces the practical reality of bridging two years between 65 and 67 using superannuation withdrawals, potential part-time work, or both. Her situation is not exceptional. It is the situation of a significant cohort of Australians whose planning was formed under one set of rules and who are now managing the transition under another.

Peter Nguyen, 66, from Melbourne, is one year away from pension eligibility and has been navigating the gap using a combination of superannuation access and reduced working hours. His experience illustrates what the new retirement transition looks like in practice. It is rarely an abrupt stop. It is more often a gradual reduction in working hours while managing drawdowns on superannuation, calibrated to reach pension eligibility age with enough remaining balance to supplement the pension income the system will then provide.

The traditional model of stopping work entirely at 65 is disappearing not just as a policy position but as a lived experience. The new reality is a more gradual transition that requires planning across a longer horizon and more financial flexibility than a single pension eligibility date required.

Superannuation in the Gap Between 65 and 67

For Australians navigating the two-year gap between the old and new pension eligibility ages, superannuation access becomes the primary financial resource for the bridging period. But accessing superannuation early in the retirement period carries long-term implications that require careful management.

Superannuation preservation age ranges from 55 to 60 depending on birth year, meaning most Australians approaching 65 in 2026 are already able to access their super under transition-to-retirement or full release conditions. The question is not whether super can be accessed but how much to draw down during the bridging period without compromising the balance that will need to supplement Age Pension income for potentially two or more decades of retirement.

Early drawdowns that deplete super to manage the 65-to-67 gap reduce the compounding investment returns that would otherwise accumulate. The two-year bridging cost needs to be weighed against the long-term income reduction that significant early drawdowns produce. For most people in this situation, a financial adviser with specific expertise in retirement income planning can model the tradeoffs with the precision that general guidance cannot provide.

The current maximum full Age Pension rate of over $1,100 per fortnight for singles, subject to income and asset tests, provides the income baseline against which super drawdown strategies should be calibrated. Understanding how superannuation income affects the income test, and therefore the pension rate, is central to optimising the combined income from both sources.

Workforce Implications for Australians in Their 60s

The policy shift has produced changes in how both employees and employers approach the final years of a working life. The abrupt retirement at 65 that characterised the previous generation’s experience is increasingly rare, replaced by a more gradual transition that has its own practical and psychological character.

Flexible working arrangements, phased retirement programs, part-time roles with former employers, and consultancy or contract work have all become more common responses to a labour market where experienced older workers are staying longer. Employers who have adapted to this reality have access to a workforce demographic with deep experience, strong professional networks, and typically high reliability, offsetting the cost of accommodating flexible arrangements.

For workers themselves, the extended working period has implications beyond the financial. Identity, social connection, and daily structure are all provided in part by work, and a more gradual exit preserves these dimensions of wellbeing alongside the income they represent. The research on retirement satisfaction generally supports the finding that gradual transitions produce better outcomes than abrupt ones for many retirees.

What Australians Approaching Retirement Should Do Now

The planning decisions made in the years immediately before pension eligibility have consequences that extend across the full retirement period, and the complexity of those decisions has increased with the shift to a 67 eligibility age and the need to manage superannuation as a bridging resource.

Confirm your exact Age Pension eligibility date based on your date of birth rather than assuming it aligns with any particular age. The staged transition means that the eligibility age for someone born in a specific year needs to be verified rather than assumed.

Review your superannuation balance and model your withdrawal strategy across the period from your anticipated cessation of work to your pension eligibility date and beyond. Understanding the interaction between super drawdowns and the Age Pension income test is essential for optimising combined income. Drawing too heavily from super in the bridging period reduces the balance available to supplement pension income for decades afterward.

Check current income and asset thresholds and understand where your projected financial position sits relative to them at the point of pension eligibility. This determines whether you are likely to qualify for the full rate, a partial rate, or potentially no pension at all depending on your circumstances, which has significant implications for how much retirement income you need to generate from other sources.

Consider part-time or flexible work as a bridging strategy that reduces superannuation drawdowns during the gap period while maintaining income, social connection, and professional engagement. The workforce increasingly supports this model, and the financial benefit of reducing drawdown pressure on super during the bridging period compounds over the full retirement period.

Consult a financial adviser who specialises in retirement income if your situation involves complexity around superannuation structure, investment assets, or planning across different income sources. The interaction between super, pension eligibility, income and asset tests, and long-term retirement income optimisation is sufficiently complex that personalised advice regularly identifies outcomes that generic guidance misses.

Frequently Asked Questions

Is the pension age going to increase beyond 67? As of 2026, no further increase beyond 67 has been legislated. However, the government review of broader retirement policy settings means that longer-term changes cannot be ruled out. Australians planning for retirement a decade or more away should monitor policy developments rather than assuming current settings are permanent.

Can Australians access superannuation before the Age Pension becomes available? Yes. Superannuation preservation age ranges from 55 to 60 depending on birth year, and most Australians approaching 65 in 2026 can access their super. The challenge is managing drawdowns to preserve sufficient balance for long-term retirement income supplementation alongside the Age Pension.

Does turning 67 automatically mean you receive the Age Pension? No. Reaching 67 satisfies the age eligibility requirement but the income and asset tests must also be met. Australians with income or assets above the applicable thresholds may receive a partial pension or no pension at all, depending on their financial position.

How has the pension age change affected workforce participation? ABS data shows that participation rates for Australians aged 65 to 69 have more than doubled over the past two decades. The change has driven both policy adaptation by employers and personal planning adjustments by workers, with gradual retirement transitions becoming increasingly common.

What is the best way to bridge the gap between 65 and 67? The most effective bridging strategies combine moderated superannuation drawdowns with some level of continued workforce participation, either part-time employment with a current or former employer or consultancy and contract work. Personalised financial advice is strongly recommended for optimising the specific combination that suits individual circumstances.