Australia Pension Age Framework From 18 March 2026: New Retirement Rules Explained

Australia’s retirement system is undergoing another significant update, and the changes taking effect from 18 March 2026 are ones that every working Australian needs to understand. The new pension age framework clarifies the rules around when Australians can access the Age Pension, tightens the eligibility requirements, and reinforces the government’s long-term strategy of encouraging people to remain in the workforce longer before drawing on public support.

Whether you are approaching retirement in the next few years or still decades away from it, understanding how this framework works will directly affect how you plan your finances, your superannuation strategy, and your retirement timeline.

What the New Framework Establishes From 18 March 2026

The 2026 pension age framework consolidates and formalizes several elements of Australia’s retirement policy that have been evolving over recent years. The key facts every Australian needs to know are straightforward.

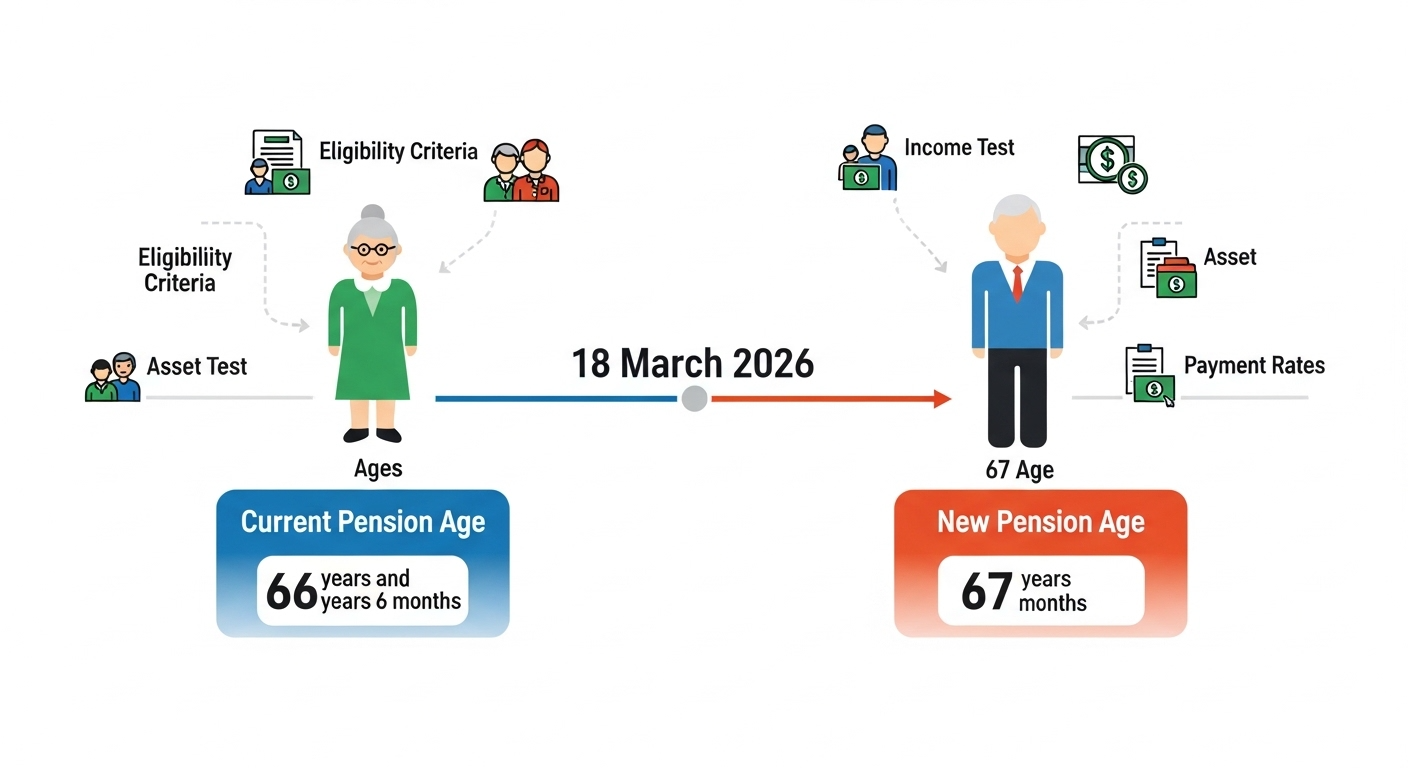

The official Age Pension eligibility age is confirmed at 67. This is the minimum age at which Australians can apply for and receive the Age Pension. There is no pathway to access the government pension earlier than this threshold under the current rules.

A minimum of 10 years Australian residency is required. Applicants must be able to demonstrate that they have lived in Australia for at least 10 years to qualify for the Age Pension. This residency requirement applies to both citizens and eligible permanent residents.

Income and asset tests remain firmly in place. The amount of Age Pension you receive, and whether you receive it at all, continues to depend on how your income and assets compare to the government’s published thresholds. These tests are applied at the time of application and reviewed regularly throughout the period you receive the pension.

The framework takes effect on 18 March 2026. Any applications lodged and any reviews conducted on or after this date will be assessed under the updated rules.

Why Australia Keeps Adjusting the Pension Age Framework

The progression of Australia’s pension access age from lower thresholds to the current 67 has been driven by one fundamental reality: Australians are living significantly longer than they were when the pension system was originally designed. A retirement that might have lasted a decade in previous generations can now stretch to 25 or 30 years. The financial sustainability of a system expected to support people for that length of time requires ongoing adjustment.

The government’s position is that aligning the pension access age with modern life expectancy is a matter of fairness across generations. Younger workers funding the pension system through taxes should not carry an indefinitely escalating burden simply because the system was designed for a different demographic reality.

Policymakers also argue that encouraging Australians to remain in the workforce longer has broader economic benefits. Experienced older workers contribute skills, institutional knowledge, and productivity that support the economy, and maintaining workforce participation for longer reduces the overall cost of the pension system over time.

Critics of successive pension age increases argue that the changes disproportionately affect people in physically demanding occupations who may not be able to work until 67 without significant health consequences. That debate continues, but the policy direction for 2026 is fixed.

How the Income and Asset Tests Work Under the New Framework

The Age Pension is not a universal payment available to everyone who reaches 67. Eligibility for the full pension, a part pension, or no pension at all depends on what the income and asset tests reveal about your financial situation.

The income test measures all regular income from sources including employment, investments, superannuation drawdowns, and other financial products. If your income exceeds the applicable threshold, your pension payment reduces at a set taper rate for each dollar over the limit. Beyond a certain income level, no pension is payable.

The assets test measures the total value of assets you own, excluding your primary residence but including investment properties, vehicles, financial investments, and superannuation balances once you reach pension age. As with the income test, exceeding the asset threshold reduces your payment according to the taper rate, and sufficiently high assets result in no pension being payable.

Both tests apply simultaneously, and the one that produces the lower payment is the one that determines what you actually receive. This means a retiree with modest income but significant assets could receive less pension than their income alone would suggest.

The specific dollar thresholds for both tests are updated periodically through indexation and policy review. Checking the current figures on the Services Australia website before you apply or before your next review is the most reliable way to understand exactly where you stand.

Key Eligibility Requirements at a Glance

The core requirements to access the Age Pension under the framework effective 18 March 2026 are as follows.

You must be at least 67 years of age. Applications submitted before reaching this age will not be accepted.

You must have lived in Australia for a minimum of 10 years, with at least five of those years being continuous residence. Specific rules apply to time spent overseas and to people who immigrated to Australia later in life.

Your income must fall within the applicable income test limits for either the full or part pension to be payable. Income above the upper threshold results in no pension entitlement.

The value of your assets must fall within the applicable asset test thresholds. Assets above the upper limit for your situation result in no pension being payable regardless of income.

You must be an Australian citizen, permanent resident, or holder of a qualifying visa at the time of application and at the time payments are made.

What This Means for People Planning Their Retirement

For Australians who are currently in their late fifties or early sixties, the 18 March 2026 framework is the rules they will be applying for the pension under when they reach eligibility age. Planning your retirement finances around these rules now rather than making assumptions will put you in a much stronger position.

Financial advisors are consistently recommending several key actions for people in the decade before retirement.

Check your superannuation balance and contribution rate now. The Age Pension is designed to supplement retirement income, not replace it entirely for most Australians. Understanding what your super balance is likely to be at retirement and whether it will be enough to carry you through your retirement years alongside or before you access the pension is essential planning information.

Model your expected income and assets against the current pension test thresholds. Many Australians discover through this exercise that they are likely to be eligible for at least a part pension, which can make a meaningful difference to retirement planning. Others discover they will be self-funded and need to plan accordingly.

Consider your superannuation preservation age. Under current rules, superannuation can be accessed from preservation age, which for most Australians currently reaching retirement is 60. This means there is typically a gap between when you can access your super and when you can access the Age Pension at 67. Planning how to fund your living costs during that gap is an important part of retirement preparation.

Speak with a licensed financial advisor well before you plan to retire. The interaction between superannuation rules, pension eligibility, income and asset tests, and tax treatment is complex. Professional advice tailored to your specific situation is worth investing in before making major financial decisions about retirement timing.

Frequently Asked Questions

What is the pension age in Australia from March 2026?

The official Age Pension eligibility age confirmed under the new framework is 67 years old. Australians cannot access the Age Pension before reaching this age under current rules.

Do income and asset tests still apply?

Yes. Both tests continue to apply and determine whether you receive the full pension, a part pension, or no pension at all. The tests are applied at the time of application and reviewed regularly throughout the period payments are received.

Can Australians access superannuation before turning 67?

Yes. Superannuation can generally be accessed from preservation age, which for most Australians currently approaching retirement is 60. Superannuation access rules and Age Pension eligibility rules are separate systems with different age thresholds.

Why did Australia raise the pension age to 67?

The increase reflects longer average life expectancy and the need to maintain the financial sustainability of the pension system over time. The change aligns pension access age with modern demographic realities while encouraging longer workforce participation.

What should I do if I am approaching retirement age?

Review your superannuation balance, check your expected income and assets against current pension test thresholds, plan for the gap between superannuation access age and pension eligibility age, and consult a licensed financial advisor to ensure your retirement plan reflects the rules that will apply when you retire.